This is part of our Inside Pavlok series—a series of blog posts by the Pavlok team talking about the story of how we work.

As the founder/CEO, my role has shifted since Pavlok’s inception. At the beginning (2013), the company was just me. I was all roles at all times. Now with 21 people (!!) on staff, my role has moved from being a doer, to being a leader.

I believe that a CEO’s job is four fold: 1) to make sure there is money in the bank, 2) to set the vision of what the product and company will become, 3) to hire the right people to get the right job done to execute that vision, and 4) to create the company culture that allows us to scale and grow in a positive and healthy way.

This article is a repost from late 2015, when we first began shipping our product. It’s fascinating for me to reread, to remember how we survived our original days pre-revenue.

I hope you enjoy this article!

-Maneesh Sethi

Yesterday, Ben Einstein of Bolt posted an article on the Bolt blog: Kickstarter is Debt.

I was in the original Bolt Class — one of the first seven companies. I was the only Bolt company (at least in the first cohort) to host a crowdfunding campaign during my tenure at Bolt, so I felt it necessary to tell our tale of Kickstarter and Debt.

Pavlok(main site, order site)was founded in 2013 with the goal of changing behavior. There are tons of wearables tracking what you do, but Pavlok is designed to change what you do. It utilizes Pavlovian conditioning (in the form of vibration or a mild electric zap) to permanently reduce cravings and break bad habits. Users use it to quit smoking, unhealthy eating, nail biting, obsessive / negative thoughts, waking up early, and more.

(and oh hey, since yesterday, we are on Amazon!)

I had the idea in late 2012, and Bolt saw our initial video and decided to invest in Pavlok and turn us into a real company. In August 2013, I accepted $50,000 from Bolt and moved to Boston, MA to pursue my goal of starting a hardware company. Now, I have no hardware experience at all — — and I was the only one there with no engineers and no experience.

While at Bolt, we accomplished the early stages that every hardware company must get through — prototyping, market analysis, and creating manufacturing partnerships.

Bolt was awesome — they even took us to China for a factory tour. Here is a video about our experience:

Debt has been in instrumental part of building our hardware company without raising a Series-A. I want to touch on Ben’s post about the Four Types of Debt — — and add a few others he didn’t mention.

How We Utilized Ben’s Four Types Of Debt

Ben discussed the four types of debt: Presales, Factory Financing, Purchase Order Financing, and Venture Debt. There are also several other forms of debt, which I write about after this section.

Here is how we utilized the four forms of debt that Ben spoke about.

Presales

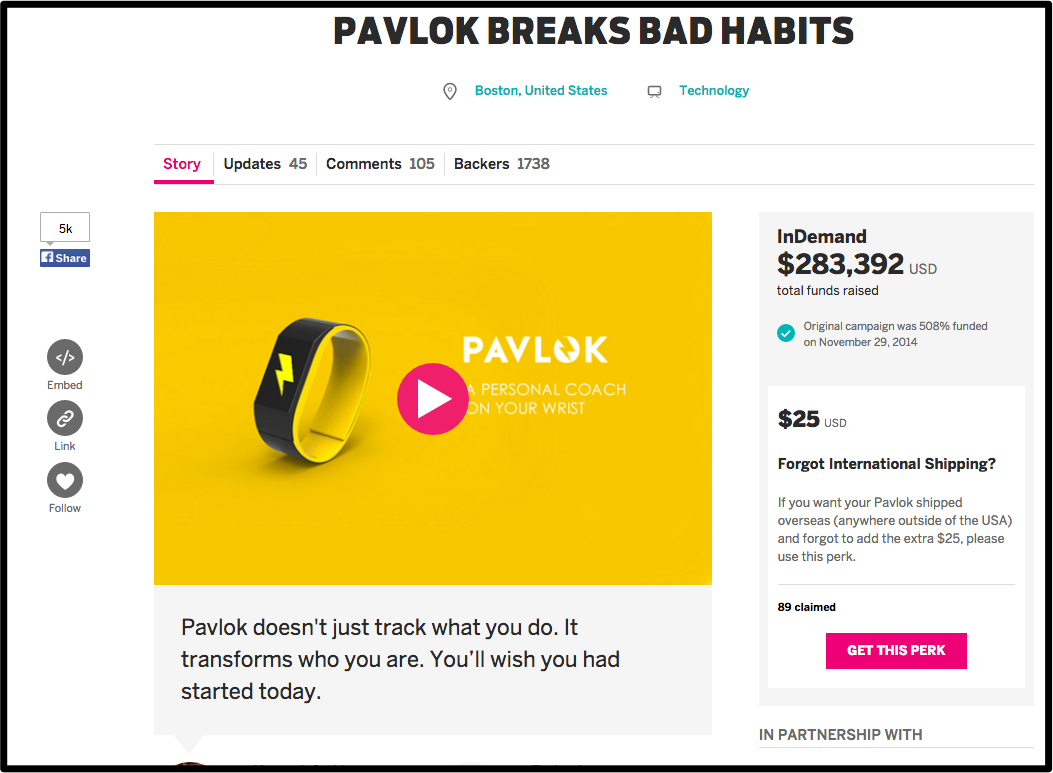

For our purposes (and you should do this too, according to Ben) we counted both our money raised in crowdfunding ($280k) and post-crowdfunding (but pre-product launch) to be “presales”.

We started our pre-sales phase well before our crowdfunding campaign. In May, 2014 we were running out of cash — — down to two weeks left in the bank. Not knowing what to do, I decided to host an informational webinar about habit formation. About 150 people showed up to this live presentation.

At the end of the presentation, I announced Pavlok and offered pre-orders. We managed to sell $20,000 in presales and prototypes on that webinar, helping us get to the next step (towards our crowdfunding campaign.

In October/November, we launched our IndieGogo campaign.

You can see the campaign at http://pavmembership.wpengine.com/igg-1

As Ben mentioned this is not “raised capital”, it is debt because we owed an individual a tangible product in return for the money given to us. Ben summed it up best in his article with this paragraph:

Like other kinds of debt, there are harsh penalties if not repaid on time (delivering late can destroy your reputation). My standard advice to consumer product founders looking to fund their companies with crowdfunding debt: use it only if you’ve completed product development (have an EP) and know your precise BOM, COGS, fixed costs and distribution margin.

It is extremely important to know what your manufacturing costs and delivery costs will be before you begin crowdfunding, or you may find that you raised an insufficient amount to deliver your product to consumers, dooming you to failure. We made the mistake of not calculating in shipping costs (particularly international) when we launched our campaign, and had to quickly backtrack and require our international customers to pay for shipping, or else we would not have been able to deliver their product. As Ben (correctly) stated:

Crowdfunding dollars should be focused on production costs (tooling, inventory, packaging, logistics) rather than development costs (customer development, prototyping, salaries).

One major irony hurt us: because these were pre-sales, they were reflected on our balance sheet as a liability, not as an asset. Thus, when we went to apply for an SBA loan in 2015, it seemed like we had LOST >$250k — — when in fact, it was cash in the bank.

This is a key tip: Pre-selling product can actually hurt your chances of getting a loan.

Factory Financing

Ben is pretty bullish on factory financing, and for good reason. It is essentially a no-cost loan. Obviously you pay for the product eventually, but you get 30, 60, sometimes 90+ days to sell that product before the money for it is due. This helps with sales and manufacturing projections, but also it is just plain useful for liquidity. Here’s Ben’s words on factory financing:

Factory financing is the most powerful form of financing for hardware companies. It usually comes as a line of credit (sometimes known as payment terms) extended by your contract manufacturer (CM). Instead of the CM requiring you to pay for parts and labor upfront, a line of credit allows you to delay that payment by 30 days or more. Unfortunately, CMs rarely extend credit to small startups during their first production run.

Ain’t that the truth. Prototyping companies typically won’t give any terms — — it’s cash up front.

We managed to get one firm to give us a $7,500 credit with net-60 terms. It wasn’t until we had proven much more sales (and had CMs competing for our business) that we managed to negotiate net terms for a greater portion of the product.

Additionally, we sourced most components ourselves. Pavlok has 80+ components, and many of them won’t allow us terms at all. With our >dozen vendors, some gave us net 30, some net 60 terms.

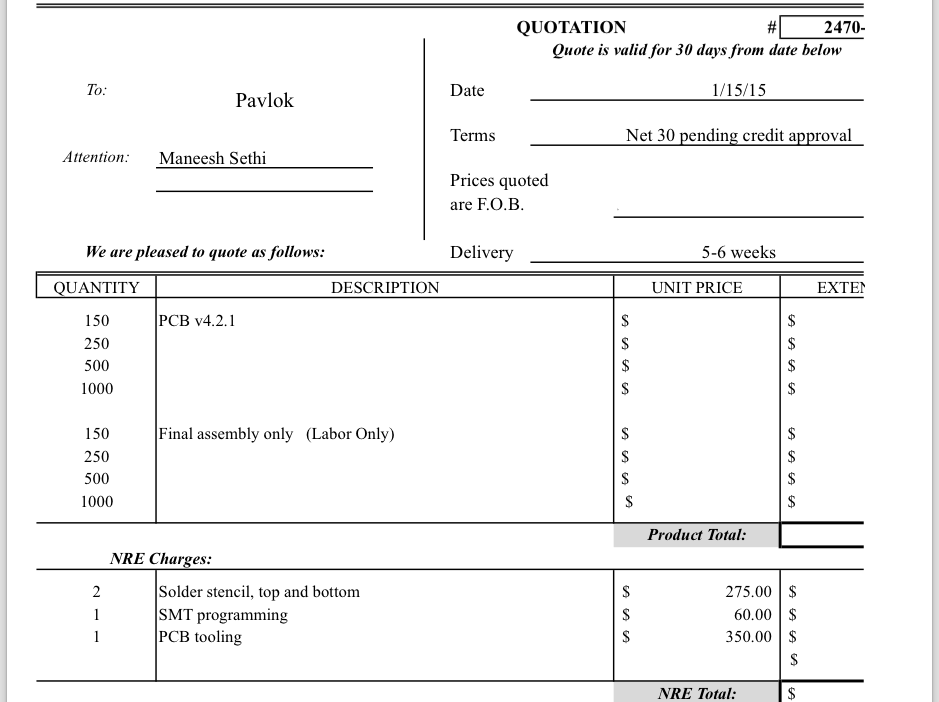

For our first production run we spent over $30k on tooling alone because we have multiple components, each requiring their own tool. Depending how large your initial production run is, financing production can be a crushing financial burden as well — for our first 18 months, we had to pay up front for all of our manufacturing.

Purchase Order Financing

Purchase order financing is a great way of financing manufacturing, if you’ve already established a sales partnership with a well known retailer. Ben describes one scenario:

If you’re lucky enough to get a significant purchase order from a brand-name retailer (or well-known B2B customer) it’s often possible to convince startup-friendly banks to provide debt financing based on pending sales. There are also financial institutions that specialize in PO financing that can be more lenient than banks. If you’re selling $2M worth of product, the lender may advance your CM $1M to manufacture the product and then collect the payment directly from the retailer. You pay for this with fees based on the amount of time between when the cash must be provided to the supplier and then the customer/retailer pays.

We had the opposite situation — instead of having a big purchase order, we had pre-sales coming through. That is, instead of having upcoming cash, we had already received the cash — — and had already spent it.

Almost every firm we approached turned us down. They said we needed an upcoming purchase order to make it happen.

After a ton of searching, we convinced OnDeck to provide us with $80k in financing (with an option to double it in the future). Inventory/PO financing is VERY expensive. They took a $2,000 initial fee. We had a factoring rate of 1.37 — — which means that we owe back 1.37x the loan, due in 11 months ($109,200). But because we make a profit on each unit, the numbers work out.

Venture Debt

Rather than betting on the potential of the business (like equity investors do) venture debt is mainly betting that your existing investors will keep financing the company. Having access to venture debt often requires investment from brand-name VCs. Often these investors will have to communicate to the venture debt firm that they have significant capital in reserve to fund the company going forward. The amount you can raise will depend on how much venture capital you’ve taken in and you’ll usually issue warrants as downside protection.

We didn’t utilize venture debt because we had very little venture capital to back it up. We tried, but venture debt firms asked us to have a Series-A arriving first. Venture Debt is typically added on as part of a VC round — — it seems unlikely to get it on its own.

Other Types of Debt(ish) Financing

There are a couple types of financing that Ben didn’t mention, that we pursued or utilized.

Bank Line of Credit

If you have a good relationship with your bank, they may extend you a line of credit. Our bank (TDBank) has opportunities for up to $150,000 in credit. A line of credit is a VERY good form of debt — — it has no costs unless you use it, and it’s only charged when you go into the red in your bank account. We were unable to secure a line of credit this year, due to our pre-sales liability situation mentioned in the Pre-sales section above.

SBA Loans

These are loans backed by the Small Business Association. Excellent loans, excellent terms, but we were unable to procure them for the same reasons above. You’ll need your business to have grossed >$50k the previous year in order to apply for a decent SBA loan.

Convertible Debt

Convertible debt is a loan that typically converts into equity at the Series-A. We raised quite a bit of convertible debt — — about $600,000 (uncapped, 10% interest, 20% discount to series A). This was done mostly through angels and friends.

Here is a guide on convertible debt.

Credit Card Debt

Credit card debt can be an effective way to gross cash when you are launching a product. Be VERY wary because obviously credit card debt can rise up and bite you in the ass. But, because we were funding a hardware product we expected to gross a lot of money on, credit cards gave us cash-flow and 30-day no-interest payment terms. I started Bolt with no debt, and probably have about $75k in debt on my cards now.

Our Total Usage of Debt

Here is a summary of our usage of debt (estimates)

- Presale

1. Crowdfunding: $280k

2. Other pre-sales: $750,000

- Convertible Debt: $600,000

- Credit Card Debt: $75,000

- Purchase Order Financing: $78,000

- Factory Financing: $7,500 (now, it’s increasing rapidly)

How Our Strategy Worked Out (Or Didn’t) For Us

What went well?

We leaned heavily on presales, and because we had a competitive advantage in our market (our advantage was that we have no competitors) it worked out well for us.

We did not have to take venture capital nor did we have to maintain an astronomical burn rate because our sales we more or less guaranteed, so long as we could reach consumers with our messaging and convey our product and brand values. We might change some of the little steps along the way (promised shipping deadlines, for example), but the strategy was a great one for us. We also didn’t have to take “real debt”, aka a bank loan, until Summer 2015, which is amazing considering we had very little venture capital. Our ability to fuel our growth through presales is one of the things we are most proud of.

What didn’t go well?

Because we weren’t venture backed and we had an unproven product, a lot of people and companies said no to us, for a lot of different reasons. We couldn’t get venture debt because we had no venture capital well to tap into in case we started running low on cash. There were some months where if we didn’t meet pre sales goals for that week or that month, we wouldn’t have been able to pay salaries let alone pay for manufacturing. That was extremely stressful, and raising slightly more venture capital would have eased some of these concerns, allowing us to focus on manufacturing issues instead of sales. This (in part) lead to our delays in shipping, which hurt presales to an extent. We learned that everything is a balance, and all parts of the business affect other parts greatly.

What we would do differently?

If we could do it all over again, we would spend more time considering our manufacturing costs and finding a manufacturer who was willing to give us net-30 or better terms. We could have dramatically reduced our presales period if we did not have to raise the funds for manufacturing through presales — if we could have product on hand to ship when it sold, it would have greatly reduced the stress that we experienced in the presales phase.

Conclusion

Hardware is hard. Everyone (well, anyone who’s done it) knows that. We succeeded because we had a unique product and aggressive sales strategies that allowed us to bring our product to market without taking large amounts of venture capital. Not taking that venture capital did close some doors for us (unable to secure venture debt, we had to struggle to pay for manufacturing costs ultimately leading to a long presales period), but we were able to overcome the challenge of creating the initial manufacturing run without giving away a large stake in the company — something we’re very thankful for now. The market you are attempting to capture will dictate what strategy is best for you. Always remember it is a balancing act: debt = obligation. Don’t take on debt without considering your COGS and overhead costs.

Are you interested in learning more about how to change behavior? Please head over to http://pavmembership.wpengine.com/email and let us know your bad habit. Or, get your own Pavlok on our site or on Amazon.

Awesome post Maneesh and valuable insights shared!